Personal Banking

-

-

Savings Accounts

Growing up with a plan for tomorrow

Shape your future

Helps you to build your nest egg

Saves you time and money

The wise investment instrument

Earn more on your Foreign Accounts

Chequing Accounts

Bank FREE, easy and convenient

A world of convenience and flexibity

Invest and enjoy the best of both worlds

A value package designed for persons 60 +

Life Stage Packages

Banking on your terms

Getting married?

Tools & Guides

Make an informed decision using our calculators

Help choose the account that’s right for you

All Our Cheques Have A New Look!

-

-

-

EBS Products

Open a deposit account online

Pay bills and manage your accounts easily

Banking on the Go!

Welcome to the Cashless Experience

Top up your phone/friend’s phone or pay utility bills for FREE!

EBS Products

Make secure deposits and bill payments

Access your accounts easily and securely with the convenience of Chip and PIN technology and contactless transactions.

Access cash and manage your money

Where your change adds up

Featured Product

-

-

-

Credit Cards

Credit Cards

Additional Information

Featured Product

-

-

-

Pre-paid Cards

-

-

-

overview

To take you through each stage of life, as we aim to assist you with the funds you need for the things you want to do

We make it easy to acquire financial assistance for tertiary education through the Higher Education Loan Programme

We make it easy, quick and affordable to buy the car of your dreams

Tools & Guides

Helps you determine the loan amount that you can afford

You can calculate your business’ potential borrowing repayments

Republic Bank's Group Life Insurance will provide relief to your family by repaying your outstanding mortgage, retail or credit card balance in the event of death or disablement.

-

-

-

Mortgage Centre

Republic Bank Limited can make your dream of a new home a quick and affordable reality

New Customers

Block for MM- new user mortgage process

There are three stages you must complete before owning your first home

Tools & Guides

block for MM - personal - mortgages

-

-

-

Investment Products

-

The Absence of the Festive Boost

TRINIDAD AND TOBAGO KEY ECONOMIC INDICATORS

| INDICATOR | 2019 | 2019.4 | 2020.4 p/e |

| Real GDP (% change) | -1.2 | -1.1 | -2 |

| Retail Prices (% change) | 1.0 | -0.1 | 0.3 |

| Unemployment Rate (%) | 4.0 | 4.1 | NA |

| Fiscal Surplus/Deficit ($M) | -4,028.9 | -386.9 | -1,040.5 |

| Bank Deposits (% change) | 5.8 | 3.1 | 2.3 |

| Private Sector Bank Credit (% change) | 4.5 | 2.9 | 1.0 |

| Net Foreign Reserves (US$M) | 9,619.3 | 9,619.3 | 10,301.1 |

| Exchange Rate (TT$/US$) | 6.73/6.78 | 6.73/6.78 | 6.72/6.78 |

| Stock Market Comp. Price Index | 1,468.41 | 1,468.41 | 1,323.11 |

| Oil Price (WTI) (US$ per barrel) | 56.99 | 56.86 | 42.50 |

| Gas Price (Henry Hub) (US$ per mmbtu) | 2.57 | 2.40 | 2.53 |

Source: - Central Bank of Trinidad and Tobago, TTSE, Energy Information Administration

p - Provisional data

e -Republic Bank Limited estimate

* - Estimate based on CBTT’s Index of Economic Activity

Overview

For many non-energy sector businesses, the fourth quarter of the year represents a period where the lead-up to Divali, Christmas and Carnival festivities normally provides a boost to commercial activity. Unfortunately, with the cancellation of Carnival 2021, the unstable job market and great economic uncertainty, (all due to the pandemic) fourth quarter 2020 was destined to be decidedly unspectacular for most businesses. Based on the available evidence, this indeed was the case, notwithstanding some encouraging performances in some industries. At the same time, the domestic energy sector continued to be hamstrung by low international prices and falling production levels. There were also additional retrenchments in the sector, as BPTT announced the departure of 149 workers in December. The company indicated that the move was in line with its parent company’s decision to restructure its global operations in accordance with the realities confronting the international energy industry. In this setting, Republic Bank estimates that activity in the domestic economy fell by 2 percent from the previous quarter. The tepid activity in the stock market was reflective of these challenging conditions, with the Composite Price Index advancing by only 0.5 percent during the period. Congruent with weak aggregate demand, price pressures remained subdued, with only a marginal rise in the rate of inflation.

Energy

Concerns surrounding energy sector production intensified late in December 2020, when it was revealed that due to the disappointing results of its infill drilling, BPTT will not be able to provide its usual supply of gas to Atlantic LNG Train 1. Train 1 usually received 100 percent of its gas from BPTT. The Minister of Energy, Mr. Franklin Khan, moved to allay fears that the Train would be shut down, indicating that negotiations were underway to secure new suppliers. He also indicated that maintenance work would be performed on the Train in January 2021. Regarding overall upstream production, gas output fell by 12.5 percent in the fourth quarter of 2020, compared to the previous quarter and by 27.4 percent year-on-year (y-o-y) to 2,525 million standard cubic feet per day (MMSCF/d). The fall in production, though linked to natural depletion in the main, was also related to maintenance work in the upstream and downstream sectors, as well as weak global energy demand. Output from the largest supplier, BPTT fell to an average of 1,248.9 MMSCF/d from 1,678.8 MMSCF/d in third quarter 2020. By comparison, the decline in oil production was mild, with the 56,109 barrels per day registered during the period, being only 1 percent lower than the figure recorded in the third quarter and 4.9 percent below fourth quarter 2019 levels. The growth of ammonia production was one of the few bright spots in the downstream sector. Output increased by 6.6 percent over third quarter levels and by 2.1 percent on a y-o-y basis. Although methanol output was 33.7 percent above the mark set in the previous quarter, it was still 29.4 percent below the fourth quarter 2019 figure. In the mid-stream sub-sector, the manufacture of liquefied natural gas (LNG) fell on both a quarter-on-quarter (q-o-q) and y-o-y basis by 29.6 percent and 42.4 percent, respectively.

Given the disappointing production outturn, the country was not able to fully benefit from the slight increase in energy prices that occurred during the period. The implications of this for government’s fiscal position and the country’s reserves of foreign currency are by now, all too familiar for most of us. During the quarter ended December 2020, West Texas Intermediate (WTI) oil prices rose to an average of US$42.50 per barrel from US$40.89 in the third. Likewise, Henry Hub gas prices increased to US$2.53 per million British thermal units (MMBTU) from US$2.

In the fourth quarter of 2020 exploration activity remained firmly below the levels recorded in the similar period a year earlier but improved when compared to the July-September 2020 period. During the period, total rig days climbed to 311 from 256 in the previous quarter but was less than the 387 posted a year earlier. Similarly, depth drilled was up 7.5 percent q-o-q but fell by 21.6 percent on a y-o-y basis.

Non-Energy

Using domestic cement sales as a proxy, construction activity expanded in the second half of 2020, after being constrained by measures designed to curb the spread of the virus, particularly in the second quarter. However, this recovery was not enough to prevent the sector from recording an overall decline for 2020. In terms of the fourth quarter, activity fell from the levels of the previous quarter but expanded significantly over fourth quarter 2019. On a q-o-q basis, the sale of cement contracted by 2.1 percent, although it increased by 19.4 percent over the same period in the previous year. The sale of new motor vehicles, which was traditionally used as a proxy for the distribution sector (now contained in the trade and repair sector) expanded by 24.4 percent over the previous quarter. This was partly owing to the rush by some consumers to acquire vehicles before the quotas and taxes announced in the 2021 Budget became effective. Nevertheless, new motor vehicle sales were 0.3 percent below fourth quarter 2019 levels. According to estimates from the Central Bank of Trinidad and Tobago, the manufacturing sector experienced a recovery in the third quarter of 2020, after being stymied by virus-related restrictions in the previous quarter. This momentum likely carried over into the final quarter of 2020. Disappointingly however, the sector’s capacity utilisation fell to 60.4 percent in the third quarter from 65 percent during the same period in 2019.

Fiscal

It must be said, that given the challenges confronting the energy and non-energy sectors, the alarm bells rung by the Minister of Finance surrounding government’s fiscal accounts were by no means a surprise. In February, Mr. Imbert revealed that for the first four months of the 2020/2021 fiscal year (October 2020 to January 2021), revenue was $1.8 billion or 13 percent short of the budgeted figure. This outturn was the result of a 9 percent ($436 million) fall in tax revenue and a 35 percent fall ($1.43 billion) in non-tax revenue. Although the decline in energy sector receipts was primarily responsible for the shortfall, non-energy revenue also declined during the period. The Minister indicated that should this trend continue, total revenue for the fiscal year would be $5 billion less than initially envisaged, leading to an actual deficit of $13.2 billion or 9 percent of GDP. In this context, government is expected to make further withdrawals from the Heritage and Stabilisation Fund (HSF), while persistent deficits will exert considerable upward pressure on public debt for the foreseeable future. In the fourth quarter of 2020, the country recorded a fiscal deficit of $1 billion and public debt ended 2020 at 82.7 percent of GDP.

Monetary

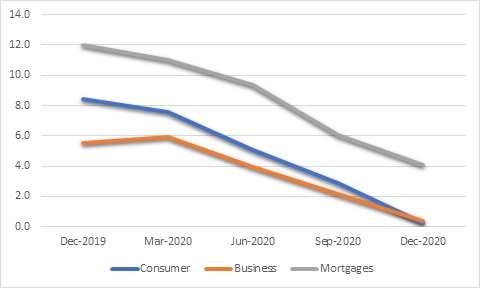

In an environment where the demand for credit was tepid and system liquidity at record high levels, the commercial banks’ average basic prime lending rate remained at 7.57 percent in fourth quarter 2020. During the period, commercial bank loans to businesses expanded by 1 percent over the previous quarter and 0.4 percent over the same period in 2019. The demand for credit among consumers was similarly unimpressive, increasing by 0.8 percent q-o-q and 0.2 percent y-o-y. Although real estate mortgage loans rose by only 0.7 percent q-o-q, they were 4.1 percent above fourth quarter 2019 levels (figure 1).

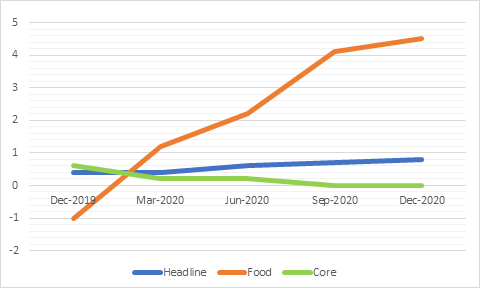

In its December 2020 monetary policy announcement, the Central Bank’s Monetary Policy Committee (MPC), maintained the “Repo” rate at 3.5 percent. The MPC cited the highly uncertain global environment owing to the pandemic, subdued domestic economic conditions and low inflationary pressures for its decision. In December, headline inflation reached 0.8 percent, marginally higher than the 0.7 percent recorded three months prior. While core prices did not advance between September and December 2020, food inflation accelerated by 4.5 percent, after a notable pick-up (4.1 percent) in September (Figure 2). The advance of food prices is partly related to international supply pressures, as adverse weather and pandemic-related disruptions affected the production of certain agricultural products. Domestic producers faced similar challenges. The MPC also highlighted that the fall of domestic interest rates have resulted in the significant narrowing of the TT-US interest rate differentials for three-month Treasuries between August and November 2020. During that time, the spread moved from 86 basis points to just 6 basis points. If the spread falls into negative territory, local investors will seek more attractive investments abroad at an increasing rate. This will increase both capital flight and foreign exchange pressures, complicating monetary policy in the process.

Figure 1: Credit Growth (% Change)

Source: CBTT

Figure 2: Inflation Rate (%)

Source: CBTT

Reserves

Given suppressed inflows from the energy sector, the market remains very tight to say the least. The outcry related to the scarcity of foreign exchange has been growing since 2014 and this issue continues to be one of the main constraints affecting non-energy businesses. With no ease in sight, one can’t help but ponder how much more challenging the situation would be when the country’s boarders are eventually opened, and/or economic activity improves, prompting the demand for foreign currency to rise above current levels. Regarding the fourth quarter of 2020, the net sale of foreign currency (the difference between purchases from and sales to the public by authorised dealers) increased by 13.2 percent over the previous quarter’s figure to US$360.8 million. However, this amount was still 9.1 percent below the outcome of fourth quarter 2019. After moves by the government to borrow on the external market and to withdraw from the HSF provided a small bump in the third quarter, the country’s stock of foreign exchange resumed its downward trend in the succeeding quarter. The net foreign position fell to US$10,308.1 million or 8.5 months of import cover (MIC) in December, from US$10,474.7 million (8.7 MIC) in September 2020. The TT-US exchange rate remained at TT$6.78 per US$1.

Outlook

The short-term prospects for the domestic economy continue to be heavily dependent on how the events surrounding the COVID-19 pandemic unfold. The rollout of vaccination programmes in several regions enhanced the prospects for the global economy in 2021 and by extension the outlook for energy prices. However, the emergence of new virus strains, new rounds of lockdowns and the uneven distribution of vaccines among countries have stoked considerable uncertainty. Nonetheless, the US Energy Information Administration forecasts oil and gas prices to average US$59.74 and US$3.26, respectively in the first half of 2021. While this is encouraging, slumping production will limit the extent to which the domestic energy sector can benefit. The non-energy sector will be challenged by lingering COVID-19 issues and ongoing foreign exchange challenges. The absence of the Carnival related stimulus in first quarter 2021 has no doubt, added to these difficulties. Overall, economic activity is expected to be flat in the first half of 2021.

Garvin Joefield

Garvin JoefieldPosted: May 4, 2021